.svg)

.svg)

October 18, 2025

AML/KYC is broken and crypto can fix it

The following is by Mesh co-founder and CCO, Adam Israel

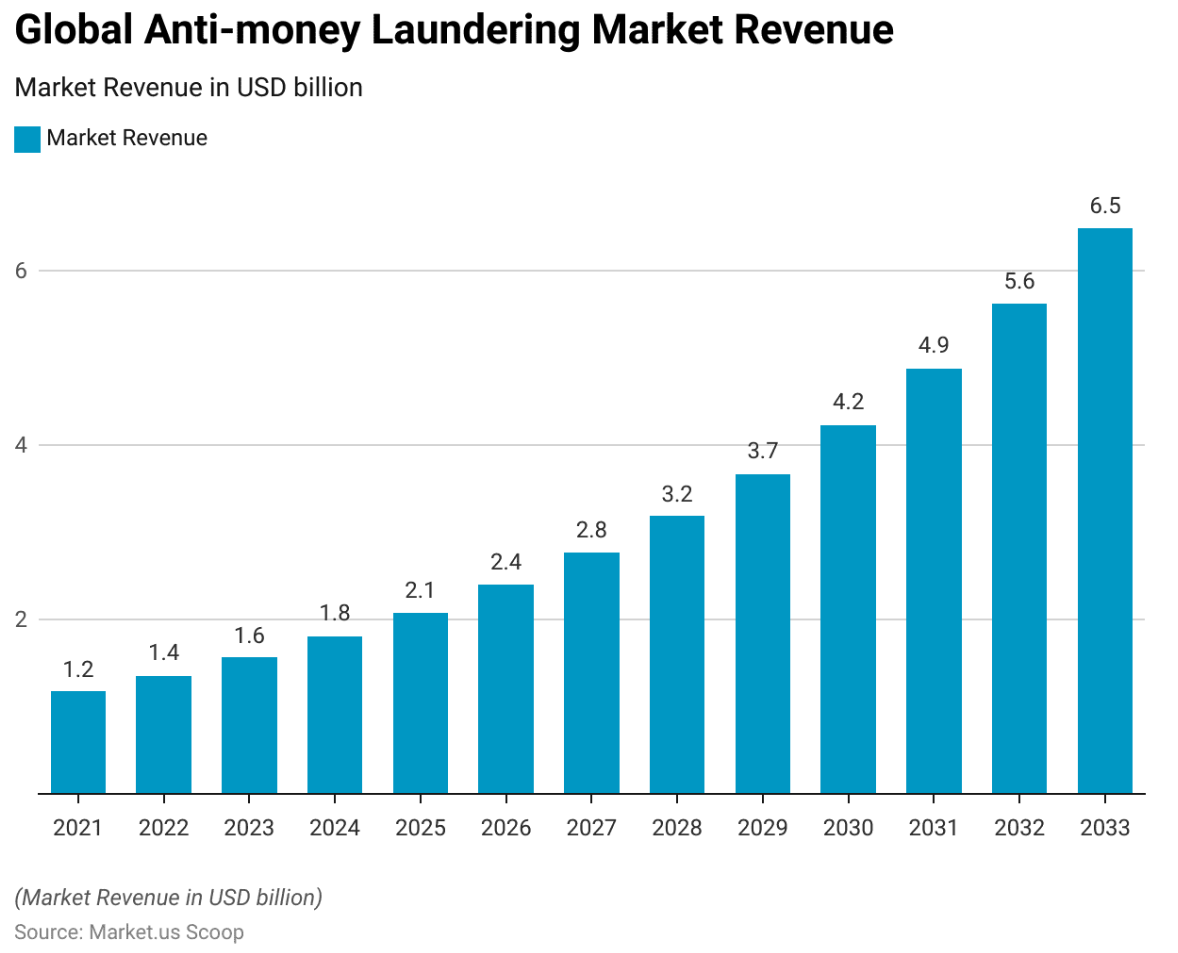

AML/KYC compliance is broken. Just this year, global spending on KYC upkeep is projected to hit a record $3B—up 12% from last year and more than double what we spent in 2021. One area where this is especially clear is the Travel Rule, which imposes new obligations on every regulated touchpoint. Banks are burning hundreds of millions annually on compliance alone, yet 95% of AML alerts are false positives and less than 1% of laundered money is actually recovered or stopped.

This is unsustainable. AML/KYC is meant to catch bad actors, not waste billions chasing false leads. We urgently need a better solution.

In this article, I lay out the problems with legacy AML/KYC and outline how blockchain tools can fix it.

Problem 1: Redundancy

A single corporate client can undergo 10+ KYC checks across different institutions. A large bank might conduct the same identity verification repeatedly, across departments and counterparties, burning resources on the same checks over and over. This isn't just inefficient, it's absurd.

These redundant processes tie up massive portions of operating budgets. Banks spend enormous amounts of money collecting the same data, verifying the same identities, and filing the same reports across fragmented systems. Meanwhile, compliance teams drown in false positives, spending countless hours chasing leads that lead nowhere.

Problem 2: Fragmentation

AML and KYC systems were built for a different era. They rely on centralized databases, siloed information, and manual reviews. When a customer opens an account at Bank A, that verification happens in isolation. If they later open an account at Bank B, they go through the entire process again. The data never travels.

This fragmentation creates waste at scale. It also exposes user data unnecessarily, as sensitive information gets copied, stored, and transmitted across multiple institutions with varying security standards.

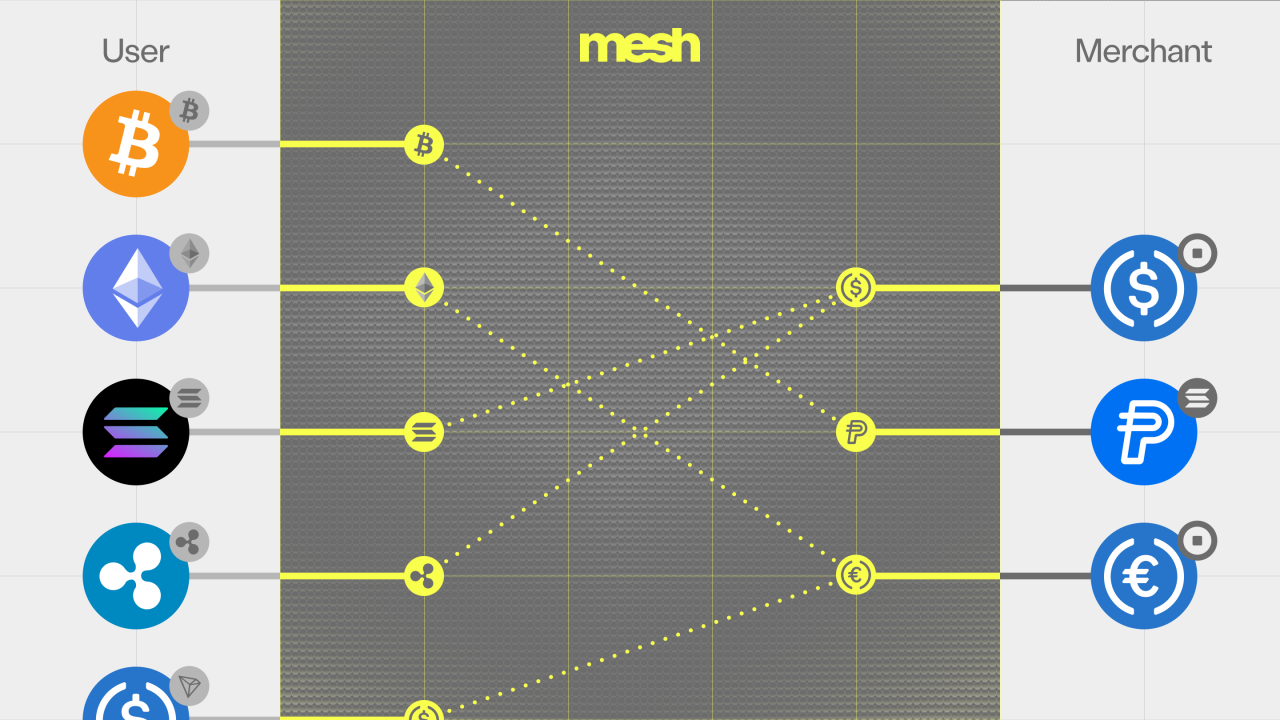

Solution: Crypto-native technology

The tools to fix broken compliance already exist. Technologies like decentralized identifiers (DIDs), smart contract automation, and zero-knowledge proofs aren't theoretical–they’re live, tested, and ready to be deployed.

At the foundation of a better system is interoperability. With DIDs and portable, verifiable credentials, users can complete ID verification once and carry that credential across institutions. This dramatically reduces redundancy. Instead of every bank or exchange repeating the same KYC process, they can simply validate the credential and move on.

Zero-knowledge proofs make this process even more powerful. They allow someone to prove they’ve passed a KYC check without revealing any personal details. No documents, no data exposure: just a cryptographic proof that’s either valid or not.

The potential impact of using crypto-native tech for AML/KYC is massive:

- Redundant ID checks could drop by up to 90%

- 97% less user data would be exposed during verification

- False positives (the biggest cost driver in AML) could be virtually eliminated by replacing rule-based detection with precise on-chain logic

The next generation of compliance should no longer rely on checklists and manual reviews, but instead be built on cryptographic trust.

Closing thoughts

AML/KYC doesn't have to be this inefficient. By redesigning compliance from the ground up using crypto-native technology, we can build a system that works for institutions, protects users, and stops financial crime.

The tools already exist. What's missing is the will to move beyond what we know and build something better.

Want more like this? Subscribe to Mesh Weekly.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

%20(1).png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)