.svg)

.svg)

April 8, 2026

Crypto Payment Gateway APIs: What Developers Need to Know (Integration, Webhooks, Security)

In 2013, BitPay signed its 10,000th merchant and processed over $100 million in Bitcoin transactions in a single year. The crypto payments era had arrived.

Within months, the first wave of developer teams ran into a hard truth: customers who owned Bitcoin struggled to send the exact amount to the right address, and a single confirmation could take anywhere from ten minutes to two days. Even Overstock, the first major U.S. retailer to accept Bitcoin, found that five years after launch - despite full CEO backing and massive press coverage - cryptocurrency accounted for just 0.2% of total sales.

The problem wasn't the technology. Blockchains work exactly as designed. The problem was that the underlying architecture of crypto payments requires new infrastructure to match the experience people expect from online commerce. That infrastructure is what payment gateway APIs provide.

What exactly is a crypto payment gateway?

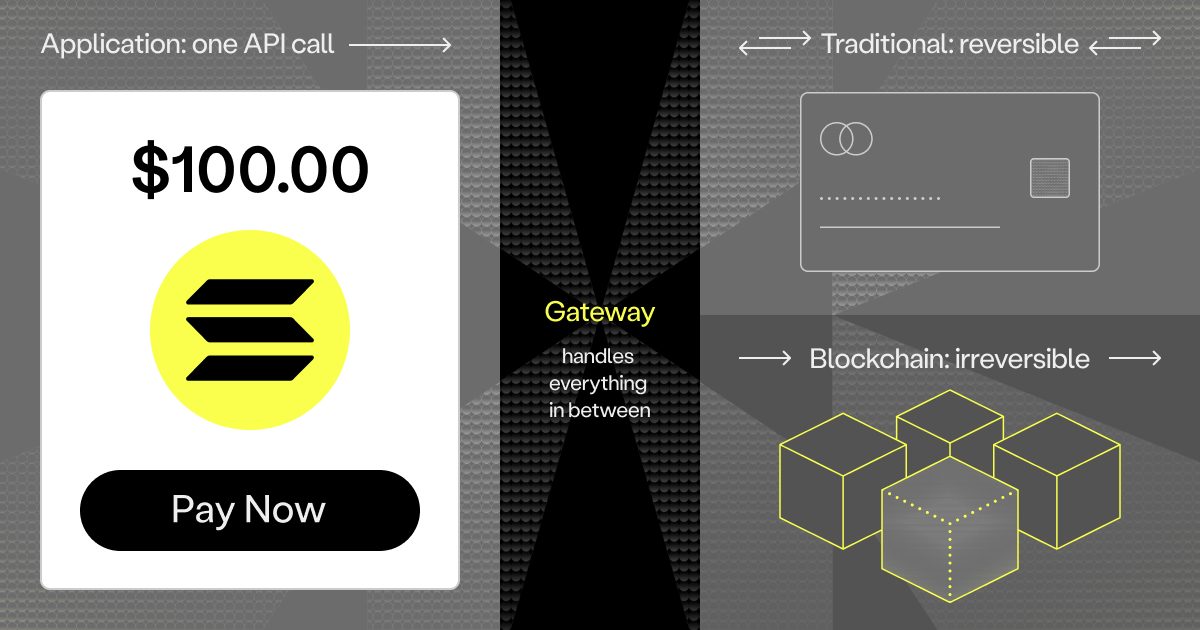

You can think of a crypto payment gateway as the layer that sits between your application and the blockchain.

It plays the same role that PayPal plays between your application and Visa's network. When a customer pays by card, PayPal handles the tokenization, fraud checks, and bank communication. You receive a webhook when payment succeeds, and you never manage card data, bank connections, or network protocols.

A crypto gateway does the equivalent: it monitors multiple blockchains for incoming transactions, handles currency conversion, and notifies your application when settlement is complete. You don’t need to operate blockchain nodes or master the consensus mechanics of two dozen networks.

But the PayPal analogy breaks down in one important way: card payments are reversible, but blockchain transactions are not. This single difference changes almost everything about how payment infrastructure works.

Where did crypto payment gateways come from?

Fun fact: the first Bitcoin payment gateway launched in 2011, two years before the word "blockchain" entered the mainstream. BitPay was built to solve one specific problem: merchants wanted to accept Bitcoin but had no way to convert it into dollars before the price moved against them.

The original solution was simple: BitPay gave merchants a Bitcoin address, monitored the blockchain for incoming funds, and settled merchants in USD automatically. That model worked when:

- Bitcoin was the only meaningful cryptocurrency

- Only one blockchain existed

- Exchange rate exposure was the primary concern

Today, however:

- Ethereum alone runs across 15+ networks

- 20+ stablecoins serve commercial payments

- Customers hold assets scattered across 300+ wallets and exchanges (which are themselves fragmented across chains and tokens)

What started as a single address and a simple Bitcoin-to-USD conversion has evolved into complex infrastructure that coordinates payments across dozens of chains, hundreds of tokens, and countless wallets.

The fundamental architectural difference

Traditional card payments work on a "pull" model. When customers enter their card details, they're giving merchants credentials to pull funds from their account. This creates fraud risk, which is why the payments industry built massive infrastructure for tokenization, fraud detection, and chargeback arbitration.

Crypto payments work on a "push" model. Customers cryptographically sign transactions to push funds to the merchant. The credentials authorizing the transfer never leave the customer's control. This eliminates credential theft but introduces a different problem: if customers send funds to the wrong address or wrong network, the money is gone.

The security model inverts. Instead of protecting against unauthorized pulls, you're protecting against irreversible mistakes.

Two ways to handle the address problem

Most crypto payment gateways generate a deposit address and hope customers copy it correctly. The customer sees an Ethereum address (42 random-looking characters), copies it to their wallet app, manually initiates the transfer, and switches back to confirm.

Each step introduces friction. Manual address entry creates three failure modes:

- Copy-paste errors send funds to malformed addresses

- Network mismatches route tokens to incompatible chains

- Address poisoning attacks exploit the habit of checking only the first and last characters.

Confirmed losses from address poisoning have reached $146M across 6,633 documented thefts–most involving users who lost between $10,000 and $100,000 to addresses that looked identical at a glance. In December 2025, one trader lost $50M in a single transaction. The poisoned address matched only the first and last characters of the real one. Nobody noticed until the funds were gone.

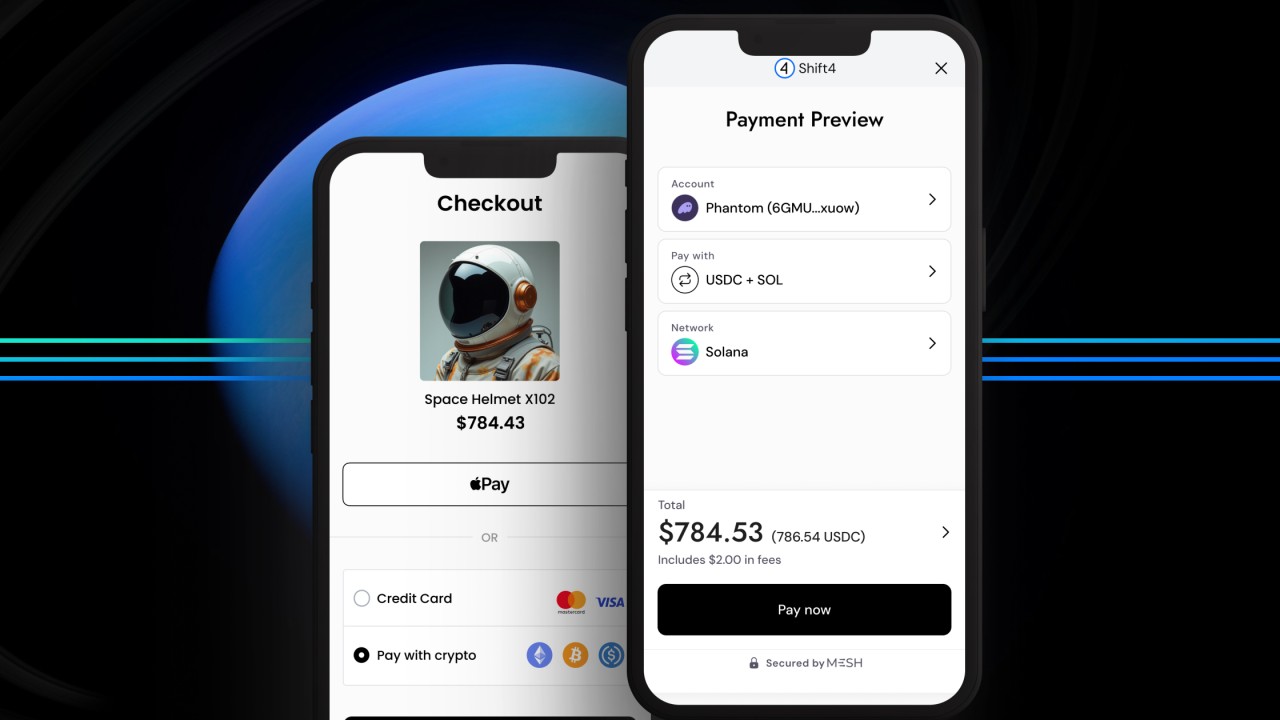

Mesh uses a different model: Authenticated connectivity

Instead of generating addresses, the system connects directly to the customer's wallet or exchange. They log in with familiar credentials (username, password, two-factor authentication), see their verified balances, and confirm the transfer. No address copying. No app switching. The transaction executes programmatically from the authenticated session.

The address problem doesn't end at checkout. Exchanges rotate wallet addresses over time, so a refund address collected at purchase may be invalid weeks later. The correct pattern: pull the refund address at purchase time for your records, but retrieve a fresh address from the exchange at refund time before initiating the transfer. With authenticated connectivity, that retrieval is a single API call.

How settlement actually works

When you pay with a credit card, settlement takes days. A transaction on Friday might not reach your bank account until Wednesday.

Crypto transactions settle in minutes to hours, depending on the network. Bitcoin requires roughly 60 minutes for recommended confirmation depth (six blocks). Ethereum settles in about three minutes (12 blocks). Solana finalizes in approximately 12 seconds. These aren’t marketing claims–they’re built-in limits imposed by how each network reaches consensus.

But settlement speed introduces complexity. A transaction appearing in a block isn't immediately final. Chain reorganizations can invalidate recent blocks when two miners produce blocks simultaneously and the network converges on one version of history. Your payment gateway must define when “confirmed” becomes “settled” based on each network’s risk of transaction reversal.

Stablecoin solve volatility but fragment liquidity

Bitcoin and Ethereum prices fluctuate too much for commercial pricing. A merchant can't accept a payment worth $100 today that might be worth $95 tomorrow. Stablecoins solve this by maintaining parity with fiat currency.

But stablecoins introduce a new problem: liquidity fragmentation.

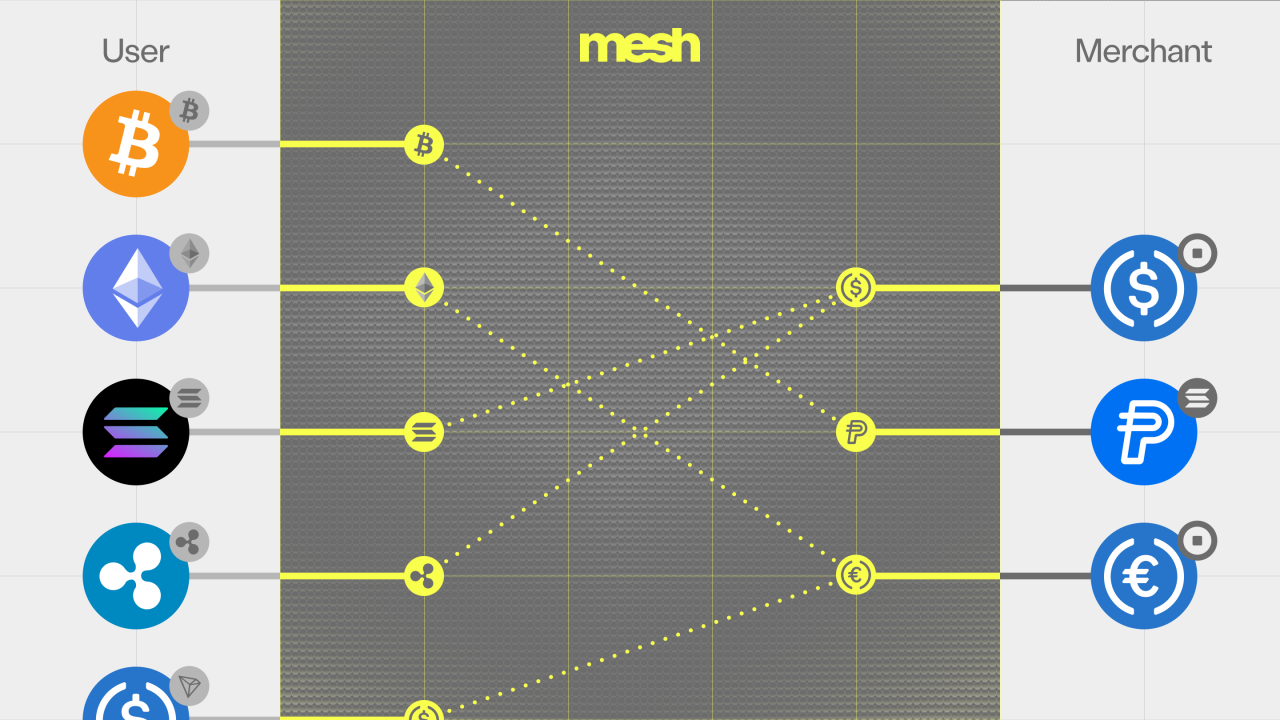

USDC on Ethereum is technically different from USDC on Polygon. They live in separate ledgers with separate contract addresses. A customer might have the right amount but on the wrong network.

Picture a customer who needs to pay $100. They have $50 in USDC on Polygon and 0.03 ETH on Ethereum. With most crypto payment systems, this transaction fails. The merchant requested USDC on Ethereum. The customer doesn't have $100 of USDC on Ethereum. Transaction declined.

This is called value fragmentation: assets scattered across accounts and networks that don't communicate. It's the digital equivalent of having enough cash to pay for dinner, but $20 is in your wallet and $40 is in your car's glove compartment.

Mesh solves this through Smart Funding, which detects available assets across connected accounts and orchestrates the necessary transfers and conversions automatically. The system routes the $50 USDC from Polygon, swaps a portion of the ETH to cover the remaining $50, and executes both transfers to the merchant's address. The customer approves a single transaction covering both sources.

This "any-to-any" payment capability is the practical result of Mesh's network architecture–300+ connected wallets and exchanges that can be orchestrated in a single API call.

Three integration patterns

You can choose from three implementation approaches, each trading off development speed for customization control.

Unless you have a strong reason to build your own UI, use the SDK. The abandonment penalty from hosted checkout compounds. Customers who leave your domain to complete payment don't come back at the same rate.

What "developer-friendly" actually means

"Developer-friendly" has become a content marketing phrase without substance. The real test is what happens when a payment fails at 2AM and your support team can't reproduce it.

Here's what actually determines whether an integration succeeds:

The gateways with the longest documentation pages are rarely the ones developers recommend.

Security considerations

Since blockchain transactions are irreversible, “security” means something different than it does for card payments. For card payments, the goal is stopping fraud. For crypto, the goal is stopping mistakes–because a mistyped address and a stolen card lead to the same outcome: permanent loss.

Your gateway must handle three critical functions correctly: validating addresses, verifying webhooks, and guarding against address-poisoning attacks.

Address validation

Before accepting any destination address, validate both format and checksum. Ethereum addresses include mixed-case characters that encode a checksum of the address hash. Validating this checksum catches typos with extremely high probability.

Different networks use different address formats. Ethereum uses hexadecimal starting with 0x, Bitcoin uses Base58Check, Solana uses Base58. Attempting to send tokens to an address format that doesn't match the network results in permanent loss.

Webhook verification

Webhooks notify your application when payments settle. Without verification, attackers could spoof these notifications and trick your system into crediting payments that never occurred.

Every webhook should include a cryptographic signature computed from the payload and a shared secret. Your handler must verify this signature before processing the event.

Protecting against address poisoning

Address poisoning exploits how people verify addresses by checking just the first and last few characters. Attackers generate addresses matching those patterns and send dust transactions, hoping their address will be copied from transaction history by mistake.

Defenses include displaying full addresses (not truncated), using address books for frequently used destinations, and implementing visual verification patterns like identicons (unique visual representations generated from the address).

Common crypto payment failures and how to handle them

Problems arise when networks become congested, fees spike unexpectedly, or transactions get stuck in the mempool.

When transactions fail

For many teams, the first issue they run into is transactions stuck in the mempool for hours over a fifty-cent fee shortfall. Customers assume their money is gone. It isn’t–but correcting that assumption at scale becomes its own challenge.

Crypto payments fail in four specific ways:

- Insufficient gas fees. Every blockchain transaction charges network fees. If the fee is too low during congestion, the transaction sits in the mempool indefinitely. Some gateways handle fee estimation automatically. Others pass this complexity to users.

- Wrong network selection. Sending USDC on Polygon to an Ethereum address generates a successful transaction on Polygon that never reaches the intended destination. The funds exist but are functionally lost.

- Chain reorganizations. A payment that appeared confirmed can become unconfirmed if a reorg invalidates the block it was in. Your system must handle payments moving backward through states (confirmed back to pending).

- Wallet connection failures. For authentication-based systems, the OAuth-style connection to the customer's exchange can time out or fail. Retry logic and clear error messaging matter.

Settlement timing expectations

"Instant" is a marketing term, not a technical specification.

Low-value consumer payments might settle after one confirmation (12 seconds on Ethereum, 10 minutes on Bitcoin). High-value B2B payments might wait for deeper confirmation (three minutes on Ethereum, 60 minutes on Bitcoin).

One operational detail catches most teams the first time: centralized exchanges batch withdrawals internally. A successful API response from Coinbase or Binance means the withdrawal is queued–not that it has landed on-chain. There can be a gap of minutes to hours between the two. Don't release inventory or trigger fulfillment on API confirmation alone. Wait for the on-chain transaction hash and your required confirmation depth.

Compliance without complexity

Regulatory compliance in crypto isn't a checklist. The rules for a $500 consumer transfer in the EU are different from the same transfer in Singapore, and both change over time.

The Travel Rule (requiring Virtual Asset Service Providers to exchange originator and beneficiary information for transactions exceeding $1,000) applies globally but with different implementation requirements by country.

Mesh handles Travel Rule compliance through intelligent provider filtering. If a transaction requires VASP ID exchange and your integration doesn't have one, the system filters out providers that enforce these requirements in affected jurisdictions. You don't track regulatory changes manually–the gateway enforces appropriate restrictions automatically.

For self-custody wallets, proving ownership involves having the user sign a message cryptographically.

Why authentication beats address generation

Address-based systems assume customers know how to use their wallets, understand network compatibility, and won't make copy-paste errors. The $146M in documented address poisoning losses is what “fail frequently” looks like in practice.

Wallet auth success doubled from 16.5% to 32.4% after Mesh improved the authentication experience–and it's still the biggest drop-off point in the flow. The pattern is consistent: auth is the hardest step. Once a user clears it, they complete the transfer.

Authentication-based systems (Mesh's model) verify account ownership first, then execute transfers programmatically. The customer logs into Coinbase or MetaMask through an embedded interface, confirms the transaction, and the system handles broadcasting. This eliminates the failure modes associated with manual address entry.

The conversion advantage compounds with user experience benefits. Customers stay in your application instead of switching to separate wallet apps, balances are verified before payment, and real-time updates track confirmation and settlement.

The production reality

The cost of not monitoring is concrete: Mesh's own internal audit found 71 client-reported issues over two months. 12 of which the team learned about from clients before internal systems detected them. That ratio is what proactive monitoring is designed to fix: knowing before your customer does.

What to monitor

Webhook delivery success rate. Should exceed 99%. If webhooks aren't reaching your server, payment confirmations don't trigger order fulfillment.

Payment completion rate. This is the percentage of initiated payments that reach settled status. It varies by integration model but should exceed 70% for authentication-based flows.

Average confirmation time by network. Compare actual timing to expected ranges. Significant deviation indicates network issues or misconfigured confirmation thresholds.

Failed payment breakdown by reason. Insufficient balance, wrong network selection, user cancellation, and timeout should each remain below 10%. Higher failure rates indicate UX problems.

When things go wrong

Blockchain infrastructure occasionally experiences issues that impact payment processing. Network congestion can push confirmation times from minutes to hours, protocol upgrades can temporarily halt transaction processing, and exchange maintenance windows can prevent authenticated connections.

Your monitoring should alert on deviations from baseline performance. If average Ethereum confirmation time jumps from three minutes to 20 minutes, you need to communicate delays to customers before they contact support.

Mesh as a reference implementation

Mesh demonstrates how to solve the fundamental challenges of crypto payment integration through specific architectural decisions.

Authenticated connectivity replaces address copying with programmatic execution from logged-in sessions. Customers connect to 300+ wallets and exchanges using familiar credentials. No addresses are copied or pasted.

SmartFunding orchestrates payments across multiple sources when a single account lacks sufficient balance. The system routes from Coinbase, converts ETH from MetaMask, and settles USDC to the merchant–all in a single user approval.

Mesh’s API works from the outcome, not the input. You specify what the merchant should receive (for example, $100 USDC on Ethereum) and Mesh figures out how the customer can pay. It calculates conversions, routing, and fees across multiple wallets and chains to ensure the exact amount arrives.

Real-time address retrieval solves the payout problem where collected addresses become stale. When disbursing to creators or gig workers, Mesh authenticates their exchange account and retrieves the current valid address programmatically.

Intelligent provider filtering handles compliance automatically. Travel Rule requirements, regional restrictions, and VASP ID verification happen behind the scenes based on user location and transaction parameters.

What actually matters

Crypto payments aren’t just card payments on a blockchain–the differences in architecture are fundamental. Cards pull funds with reversible authorization and settle in days through centralized clearing. Crypto pushes funds with irreversible finality and settles in minutes across fragmented networks. Cards fail from fraud; crypto fails from user error.

These aren’t minor details–they define which integration patterns succeed. Address-based flows assume users understand network compatibility; authentication-based flows remove that assumption. Manual bridging expects users to handle cross-chain complexity; SmartFunding eliminates it. Mesh solves these challenges architecturally: authenticated connectivity replaces error-prone address copying, SmartFunding orchestrates payments across fragmented accounts, and settlement-based input lets developers specify what they want to receive, not what users need to send.

Ultimately, choosing the right gateway is more than a technical decision–it determines how effectively you can navigate crypto’s unique constraints, deliver a seamless customer experience, and realize the full business potential of digital payments. You should invest in the gateway that lets your business scale with confidence.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

%20(1).png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)