.svg)

.svg)

March 21, 2026

Why Payment Settlement Speed Matters for Crypto Merchants

The following is by Mesh Counsel Damilola G. Arowolaju

Most people think of payments as instantaneous. You tap a card, send a wire, or move money between accounts, and take for granted that it’s not an instant transfer.

Beneath the surface, money rarely moves in real time. It waits. It lingers. It sits in transit between institutions for hours or days at a time.

Delay is unfortunately a feature, not a bug.

In this article, I demonstrate how delay is monetized and how incorporating stablecoins into payments offers a better alternative.

Time is money

In modern finance, delay is a business model. Wherever money lingers, firms profit.

Consider a landscaping company that receives a $3,200 client payment on Monday. Payroll debits Tuesday but the payment doesn’t clear until Wednesday. The account then overdrafts not because the business is insolvent, but because the money is still in transit. The $35 fee goes to the bank.

This seemingly absurd scenario reflects the daily reality of a system where settlement is measured in days not seconds. Entire industries are built around slowing the movement of money:

- Insurance companies extend claims timelines to capture float and defer payouts.

- Payroll providers hold wages and earn overnight interest on billions in aggregated deposits.

- Correspondent banking routes a single wire through multiple intermediary banks, each taking a cut while holding the float.

To end users, these inefficiencies are unjustifiable. But to the intermediaries who profit, they’re revenue streams.

→ For a deeper look at how this affects corporate finance, read how stablecoins will reshape corporate treasuries.

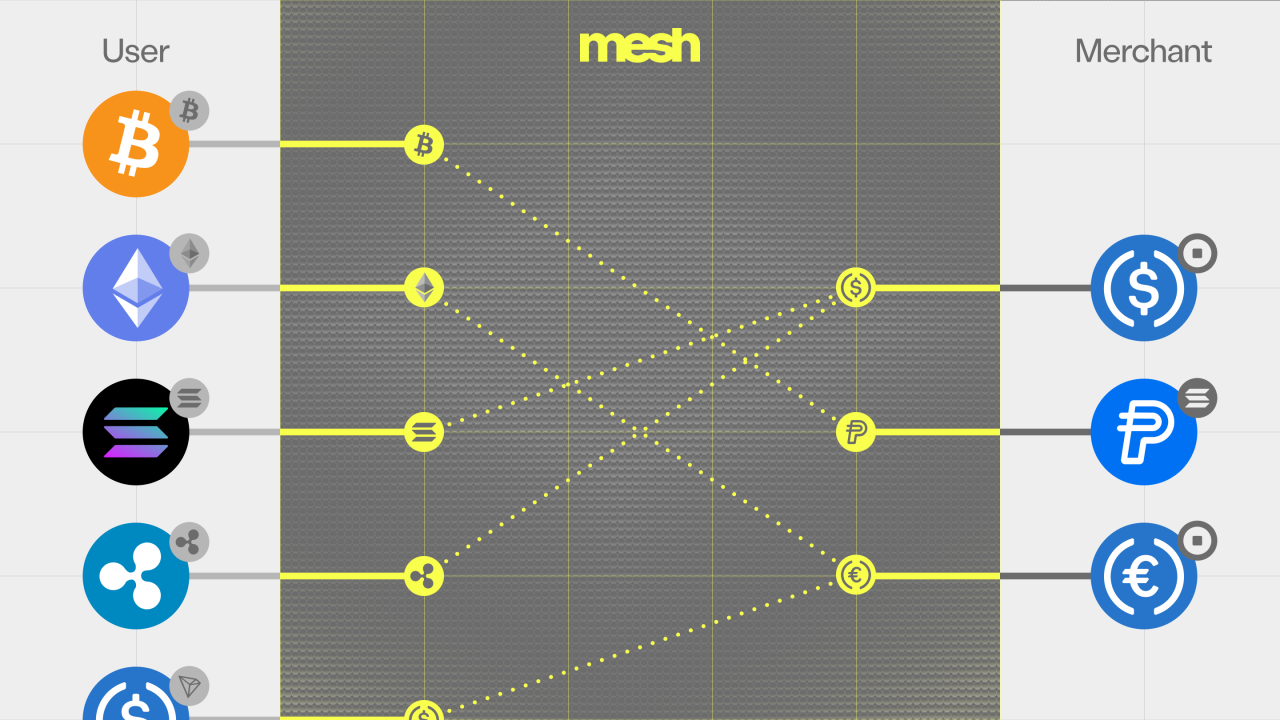

The stablecoin solution

Stablecoins are a direct response to this system of monetized delay. By design, they strip intermediaries of the ability to profit from slow settlement. Transactions clear continuously (not in batches, like ACH) and float vanishes. As a result, time is no longer a source of revenue extraction.

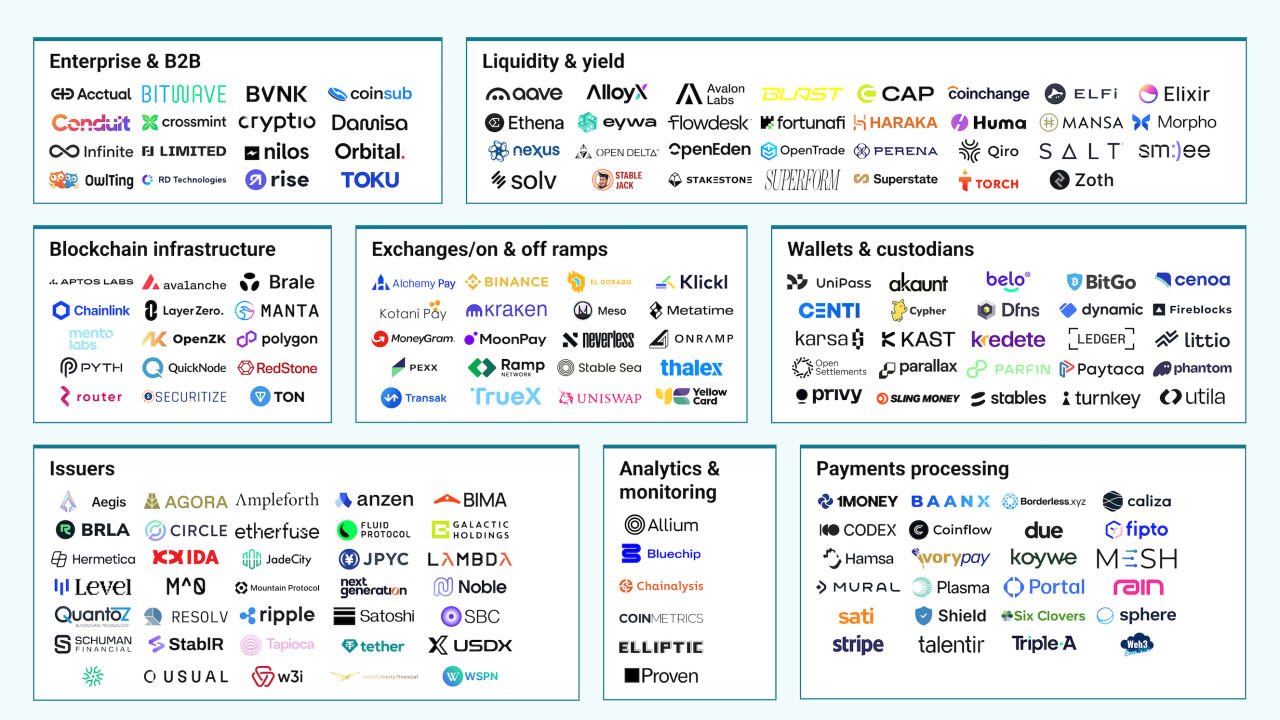

The market is already validating this shift. Following the passage of the GENIUS Act, major financial institutions, card networks, and fintech platforms began integrating stablecoins into their systems. Stablecoin supply reached roughly $311B at the end of 2025, with transfer volume hitting $11.6T. Forecasts from Jefferies, Citi, and JPMorgan all point to continued growth into the hundreds of billions (if not trillions) over the coming decade.

Adoption is accelerating because the incentive is simple: faster money benefits both the sender and the receiver. The only parties worse off are the intermediaries depending on delay.

Closing thoughts

Stablecoins introduce a brand new payment model: money moving at the speed of the internet and value accruing to the participants in the transaction rather than the intermediaries. There’s still much more progress ahead, and the economic impact won’t flow evenly. In the short term, efficiency gains will likely benefit cross-border payments the most, where delays and fees are historically the highest.

Over time, however, the implications will extend far beyond payments. As settlement becomes instant and continuous, financial systems will begin to resemble the internet itself: always on, globally accessible, and indifferent to borders.

In that world, delay is no longer something to monetize.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

%20(1).png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)