.svg)

.svg)

May 15, 2026

The Best Crypto Payment Solutions for Enterprise in 2026: What Actually Matters

The enterprise conversation about crypto payments has changed. Two years ago, most procurement decks asked one question: does it work? Today, the question is whether the infrastructure underneath can survive a Black Friday traffic spike, a Travel Rule audit, a treasury policy review, and a CISO security questionnaire — in the same quarter.

The answer separates real enterprise infrastructure from accept-crypto plugins dressed up for the enterprise buyer. This guide breaks down the five capabilities that actually distinguish enterprise-grade crypto payment solutions in 2026: scalability under real load, security and compliance built in (not bolted on), broad connectivity across the crypto stack, intelligent orchestration that removes volatility from the merchant's books, and verified wallet ownership for every counterparty.

Why "enterprise crypto payment solution" is a higher bar than it used to be

Stablecoins crossed $300B in market cap in 2025. But the more instructive number is the real-world payment volume underneath the trillion-dollar headline figures: McKinsey and Artemis Analytics found that actual stablecoin payments hit roughly $390 billion in 2025, double the 2024 figure, with B2B payments alone growing 733% year-over-year. That's the slice of stablecoin activity that represents enterprises moving real money — vendor payments, payroll, remittances, capital markets settlements — and it's the part scaling fastest.

Enterprises aren't piloting crypto rails anymore — they're depending on them for revenue, payouts, and treasury operations. That shift changes the requirements:

- Volume: payment platforms need to process spikes without queuing, dropping, or repricing mid-transaction.

- Multi-region: customers and counterparties live in 100+ jurisdictions, each with its own regulatory regime.

- Asset and account diversity: the average crypto holder owns assets across multiple accounts, chains, and exchanges. Limiting acceptance to one network, one account type, or one token loses transactions.

- Auditability: finance and compliance teams need clean reporting, not a CSV export from a block explorer.

An enterprise crypto payment solution has to clear all four bars at once. Most consumer-grade providers clear one or two.

The five capabilities that define enterprise-grade crypto payments

1. Scalability that holds under real volume

Throughput claims are easy to publish. Throughput under load is the harder problem. Enterprise platforms need to handle bursty traffic — promotions, market events, end-of-quarter payouts — without degraded latency, retry storms, or settlement delays that show up as customer complaints two days later.

Mesh's network has been built on this principle from day one. Mesh's $82M Series B in March 2025 was settled largely in stablecoins on its own rails, with PayPal Ventures' earlier strategic investment partially settled the same way — institutional-scale value transfer in production. The platform powers payments, deposits, and transfers reaching more than 900 million users across over 100 countries, meaning the load it's already proven against isn't theoretical.

The architectural choice that makes this possible: Mesh sits as a routing and orchestration layer above the underlying networks rather than constraining payments to a single chain. When one network is congested, traffic moves. When a new chain becomes the cheapest path, traffic follows. Enterprises don't have to re-architect their integration to capture those gains.

2. Security and compliance by design

Enterprise security is not a marketing page. It's a stack of attestations, controls, and engineering decisions that hold up to a written questionnaire from the customer's CISO.

Mesh is SOC 2 Type II and ISO 27001 certified. Both certifications matter for different reasons — SOC 2 Type II validates that security controls operate consistently over time, not just at a point-in-time audit, and ISO 27001 validates the broader information security management system. Together they're the two attestations enterprise procurement teams ask for first.

Compliance is the second half of the same equation. Mesh's approach is compliance-by-design — meaning regulatory requirements aren't added as a wrapper around the product, they shape the product's primitives:

- MiCA and EBA Travel Rule alignment is built into the verification flow, not handled by a third-party plugin.

- Wallet ownership verification is completed before funds hit the platform — not after. Most solutions check ownership only once assets have already arrived, which leaves the institution to freeze and investigate after the fact. Mesh's signed-message attestation runs at connection time, returning the cryptographic proof (message hash, signature, wallet address) to the client before the transaction completes.

- KYC identity matching through connected exchange accounts lets platforms confirm counterparty identity without re-running KYC the user has already completed elsewhere.

The result for an enterprise: a single integration that satisfies the EU Travel Rule, supports MiCA-aligned attestation, and produces audit-grade records — without each capability requiring a separate vendor.

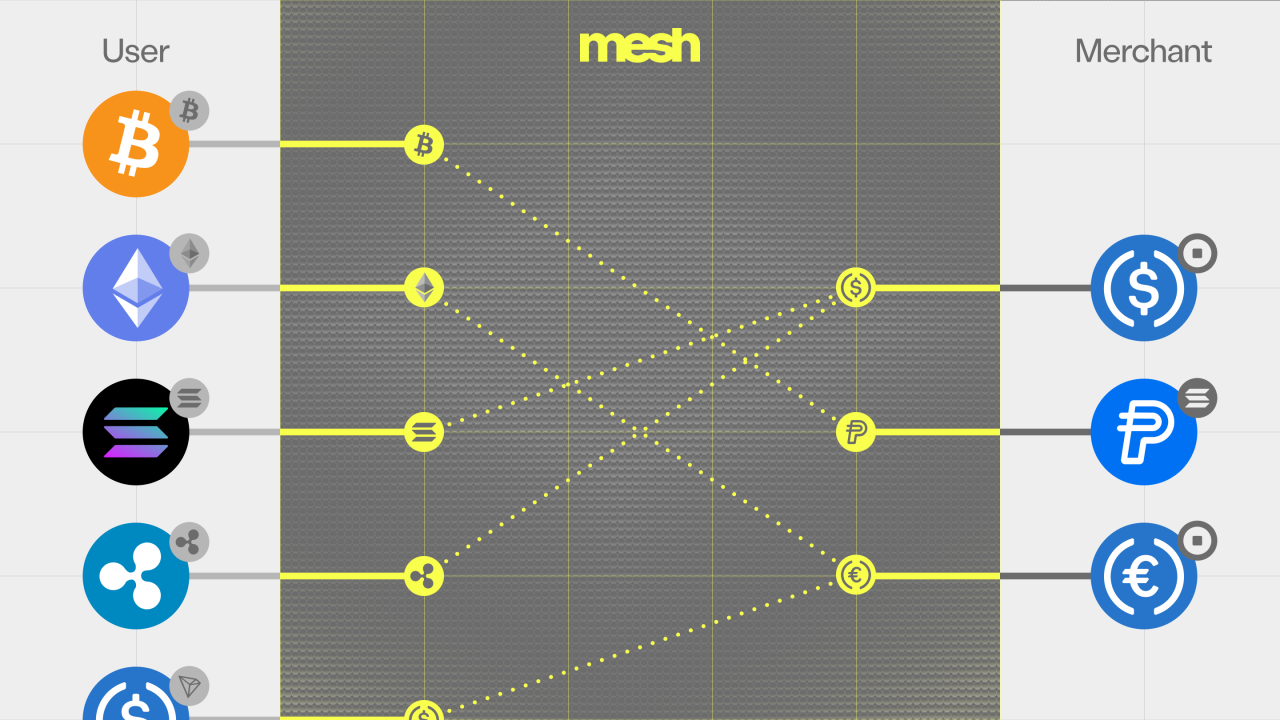

3. Broad connectivity to the entire crypto stack

The defining problem of crypto payments at enterprise scale is fragmentation. Customers hold assets across 300+ wallets and exchanges, spread across dozens of chains and 20+ stablecoins — and they hold the volatile tokens too. A payment solution that only supports one chain, one account type, or one token category loses every transaction that doesn't match.

Mesh connects to 300+ wallets, exchanges, and platforms — including Coinbase, Binance, MetaMask, Phantom, Bybit, OKX, Uphold, and the long tail of regional venues — through a single integration. Coverage spans 120+ supported tokens across 24+ networks, including the major volatile assets (BTC, ETH, SOL) and the full set of stablecoins enterprises actually settle in.

Connectivity isn't just inbound. The same network connects to the settlement assets and rails enterprises want to land on — the customer or partner picks the stablecoin and the network they want, and the routing handles the rest.

4. Intelligent orchestration for any-to-any payments

This is where a payment network becomes infrastructure rather than a connector. Intelligent orchestration means routing each transaction across the right combination of wallets, chains, conversion venues, and settlement layers automatically — based on cost, speed, success probability, and counterparty trust — without forcing the user to think about any of it.

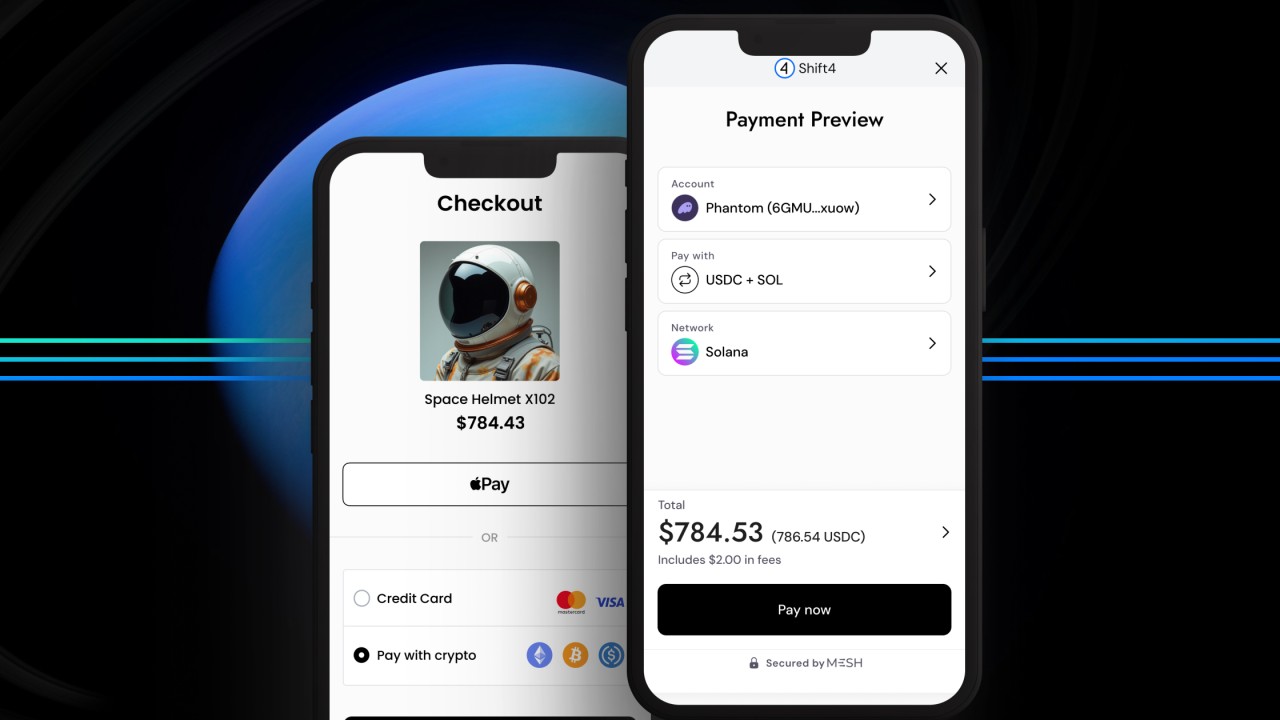

Mesh's SmartFunding is the orchestration layer that enables true any-to-any payments. The customer pays with any asset they hold (Bitcoin, Ethereum, Solana, any major stablecoin on any supported chain). The merchant receives instant settlement in their preferred currency — USDC, PYUSD, USDT, or local fiat. The routing decision happens in real time, in the background, based on the most efficient path available at that moment.

The mechanism: SmartFunding can combine up to five funding sources within a connected account — existing crypto balance, crypto-to-crypto conversion, stablecoin conversion, buying-power purchase, and linked payment method — into a single transaction the user experiences as one tap.

5. Wallet ownership verification that satisfies regulators and protects revenue

For any enterprise dealing with self-hosted wallets — which today means most of them — ownership verification is now table stakes. The EBA's Travel Rule Guidelines and MiCA both require crypto-asset service providers to verify that the wallet a customer is transacting from actually belongs to that customer. Failing to verify doesn't just create regulatory risk; it creates fraud risk on every inbound payment.

The architectural point that matters most: ownership is verified before funds enter the platform. Most verification solutions confirm ownership after the deposit lands, which means the operations team is left to freeze, investigate, and unwind transactions on a regular basis. Mesh runs verification at connection time — the user signs the specified message inside their wallet, Mesh returns the signed message hash, signature, and wallet address to the client, and the transaction proceeds only once the cryptographic proof is in hand.

Mesh supports multiple verification methods so enterprises can pick what fits their flow:

- User attestation via signed message — gasless, embedded, MiCA- and EBA-aligned. The method Revolut runs in production across the EU under MiCA, processing thousands of verifications daily.

- KYC identity matching — for verifying users connected through centralized exchanges, by matching identity data from the connected account.

Both methods run inside the same flow as the payment or deposit, so verification doesn't add a separate step the user can drop off in. Revolut integrated Mesh's verification specifically for this combination: compliance with the EU Travel Rule plus enterprise-grade verification for self-hosted wallet ownership, delivered without breaking the existing UX.

How to evaluate a crypto payment solution for enterprise

Cut through the marketing pages with a short evaluation checklist:

- Audited security: ask for the SOC 2 Type II report and ISO 27001 certificate, not a security overview deck.

- Compliance scope: ask which specific regulatory frameworks the platform supports natively — MiCA, EU Travel Rule, FinCEN, MAS — and which require third-party add-ons.

- Connectivity breadth: count wallets, exchanges, chains, and stablecoins supported through the single integration. Then ask which of those the platform has actually transacted on at volume in the last 90 days.

- Orchestration depth: ask the provider to walk through a real transaction where the customer's source asset and chain don't match the merchant's settlement currency. The right answer involves real-time conversion and routing in the background, not a manual user step.

- Settlement flexibility: confirm support for the specific stablecoins and fiat currencies the business needs to settle in, today and on the 12-month roadmap.

- Verification timing: confirm that ownership is verified before funds arrive on the platform, not after. The difference shows up in the operations team's workload.

Who's already using Mesh in production

The proof points enterprise buyers look for first:

- PayPal — Mesh powers the infrastructure behind PayPal's Pay with Crypto service, with PayPal Ventures an early strategic investor.

- Shift4 — Mesh enables Pay with Crypto across Shift4's merchant base globally, with crypto transactions converted into local currency at the point of sale.

- Revolut — Mesh's verification infrastructure runs in production across Revolut's EU operations under MiCA.

- Kalshi — Mesh enables deposits and payouts across 300+ wallets and exchanges for the first federally regulated prediction market, contributing to 138% deposit growth.

Frequently asked questions

What's the difference between a crypto payment processor and a crypto payment network?

A processor handles a payment for one merchant on one set of rails. A network — like Mesh — sits across wallets, exchanges, chains, and settlement venues and routes each transaction across the most efficient combination available. Networks make any-to-any payments possible; processors make one-to-one payments possible.

Does an enterprise need a separate provider for stablecoin settlement?

Not with a network model. Mesh settles in USDC, PYUSD, USDT, and local fiat through a single integration. The merchant picks the settlement currency and the network; the network handles the conversion at the point of transaction.

How does Mesh handle volatility risk for merchants?

Settlement happens in the merchant's chosen stable asset or fiat at the time of transaction. The customer pays with whatever they hold; the merchant never holds the underlying volatile asset on their books.

Is Mesh compliant with the EU Travel Rule?

Yes. Mesh's signed-message attestation and KYC identity matching satisfy MiCA and EBA Travel Rule requirements. Revolut runs Mesh's verification infrastructure in production across the EU.

How many wallets and exchanges does Mesh connect to?

300+ wallets, exchanges, and platforms today, covering 120+ tokens across 24+ networks — with continuous expansion across regions including Latin America, Asia, and Europe.

What's next

The enterprise crypto payments bar is higher than it used to be — but the infrastructure to clear it exists. Mesh powers crypto payments, deposits, and verification for PayPal, Shift4, Revolut, Kalshi, and partners across more than 100 countries.

Building or evaluating? Read the developer docs →

Ready to talk? Get in touch with our team →

.png)

.png)

.png)

.png)

.png)

.png)

.png)

%20(1).png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)