.svg)

.svg)

July 16, 2026

Account Funding for Banks: How Customers Fund an Account with Crypto

When a customer wants to move crypto into a bank, the intent is the easy part. The money is scattered across wallets, exchanges, tokens, and networks — and any mismatch (wrong network, wrong asset, not enough in one place) makes the deposit fail or sends the customer to an external tool they don't come back from. Account funding is how a bank lets a customer fund an account from any of those sources — a wallet, an exchange, or an on-chain balance — and receive it in the institution's preferred asset, with the connection, conversion, and routing handled through one integration so the deposit actually completes. Mesh powers this with SmartFunding, turning external crypto into deposits that land in the bank's chosen asset. Mesh isn't in the flow of funds.

The goal is to remove the complexity for both sides. A customer picks a source and an amount; the funding layer handles connection, ownership checks, and any conversion, so the funds arrive in the institution's preferred asset.

Not legal or compliance advice. This article explains how the capability works. Requirements vary by jurisdiction and institution; validate against your own compliance and legal review.

What is account funding?

Account funding is the capability that lets a bank's customer add money to their account from an external source — a bank transfer, card, exchange balance, or crypto wallet — and have it arrive in the institution's preferred asset. For crypto, that means accepting any supported token from any connected source and converting it, behind the scenes, into the bank's designated asset. The same capability is sometimes described as deposit funding orchestration or multi-source funding infrastructure; the job is identical — turn whatever a customer already holds into a completed deposit.

Instead of building a separate funding path for each source and each asset, the bank offers one "fund your account" flow and lets the funding layer resolve the details underneath.

What problem does it solve for banks?

Most crypto deposits fail on avoidable friction. A customer picks the wrong network, pastes the wrong address, doesn't have the full amount in one place, or gets bounced to an external wallet tool mid-flow and never returns. For the bank, every failed or abandoned deposit is external crypto that never became a managed asset.

Account funding removes that friction in three ways: it combines multiple funding sources within the customer's connected account — different tokens, or a linked cash balance — so a deposit can complete even when no single asset covers the full amount (funding source aggregation); it validates the network and asset before anything moves, so deposits don't fail on mismatches; and it keeps the whole flow embedded in the bank's own experience instead of redirecting out. The result is more completed deposits — more external crypto converted into assets the bank manages.

How does crypto account funding work?

Three coordinated steps, with Mesh coordinating them at the connectivity layer.

1. Connect and verify the source. The customer connects a funding source from Mesh's network of 300+ wallets and exchanges, and ownership is verified before anything moves — a verified deposit.

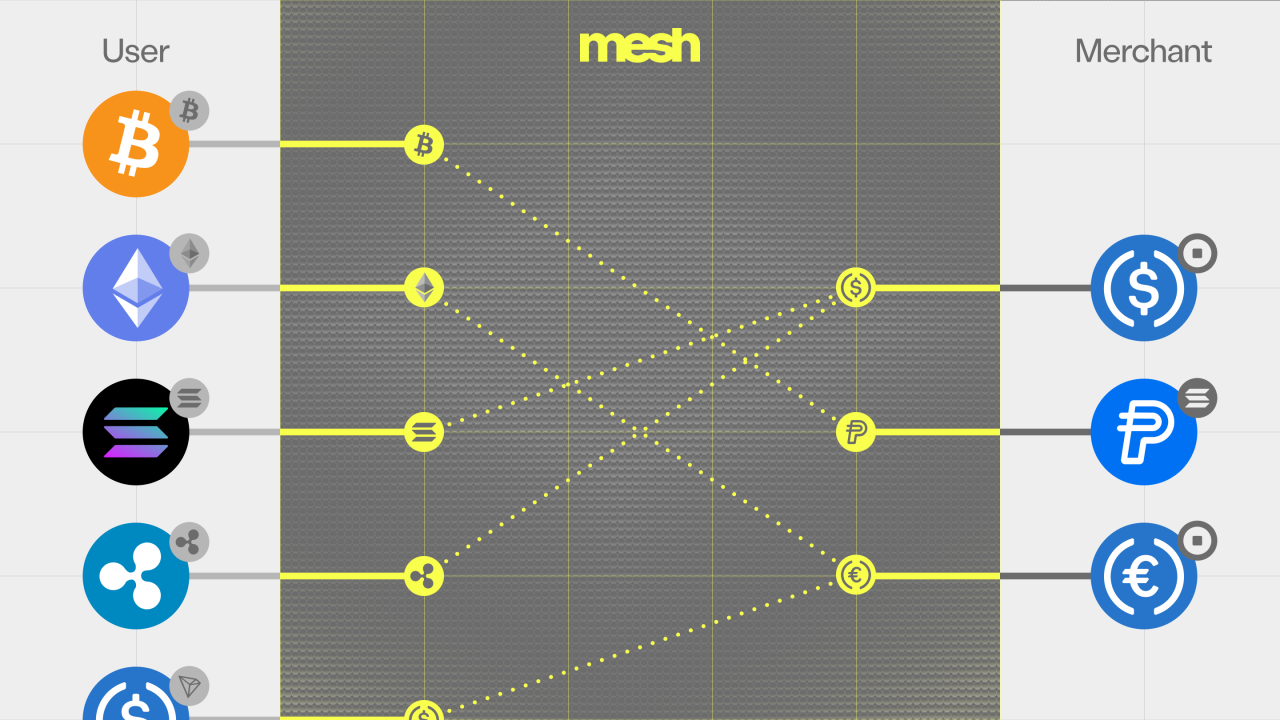

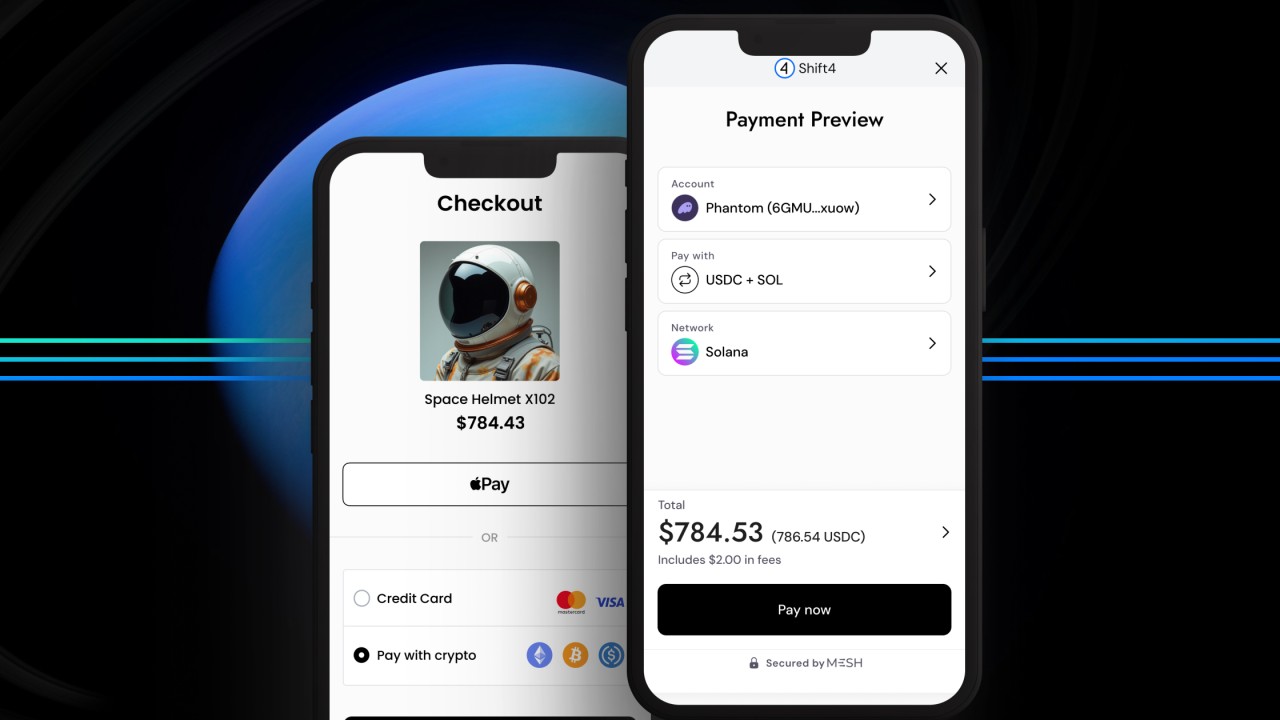

2. Combine, convert, and route. SmartFunding combines the customer's available balances within the connected account, converts any supported asset into the institution's preferred asset, and determines the path — so a customer can fund in one asset and the bank receives another (for example, a stablecoin).

3. The deposit lands. The customer's exchange or wallet executes the transfer on their authenticated instruction, and funds move directly from the connected source to the institution. Mesh passes the instruction and tracks the transfer — it never touches funds in flight.

How does SmartFunding increase deposit success?

SmartFunding is Mesh's engine for making deposits complete. It combines multiple funding sources within a customer's connected account in real time — different tokens, or a linked cash balance — so a deposit can complete even when no single asset covers the amount, converts whatever the customer funds with into the bank's preferred asset, and handles path selection behind the scenes — reducing failed "insufficient funds" deposits and keeping the experience inside the bank's own experience rather than a redirect. In the institution's terms, that means more of a customer's external crypto actually lands as a deposit.

What makes it different?

Coverage and completion. Mesh's network spans 300+ wallets and exchanges through API-level integrations — not aggregation — so one integration reaches wherever customers already hold assets. And SmartFunding is the only system that combines multiple funding sources in real time to complete deposits that would otherwise fail, converting whatever the customer holds into the institution's preferred asset behind the scenes. Mesh is the orchestration and instruction layer throughout — it passes the customer's authenticated instruction to the platform that executes the transfer. The customer sees one "fund your account" flow; the complexity stays in the layer.

Which sources, assets, and networks does it support?

Account funding draws on Mesh's network of 300+ wallets and exchanges as sources and supports 120+ tokens across 24 networks, including the mainstream stablecoins (USDC, USDT, USDG, PYUSD, RLUSD, EURC) institutions commonly choose to receive, and major tokens (BTC, ETH, SOL) as funding assets.

Who is already using it?

AMINA Bank, the Swiss FINMA-regulated crypto bank, integrated Mesh so clients can fund from a connected wallet and have the deposit arrive in the bank's chosen asset — conversion handled at the point of deposit, inside the bank's own platform.

Paxos, the regulated blockchain-infrastructure and tokenization platform, integrated Mesh so the institutions it serves can offer verified funding from external wallets and exchange accounts to their own customers, including for assets such as PYUSD and USDG.

Where does account funding fit in a bank's digital asset stack?

Account funding sits on top of connectivity and verified deposits: connectivity reaches the sources, verified deposits prove control of them, and account funding aggregates, converts, and completes the deposit across them. The engine is SmartFunding. For how all three layers assemble into a launch-ready stack, see digital asset infrastructure for banks.

Frequently asked questions

→ What is account funding? The capability that lets a bank's customer add money to their account from any source — bank transfer, card, exchange, or crypto wallet — and receive it in the institution's preferred asset, through a single integration.

→ What is deposit funding orchestration? Another term for the same capability: coordinating connection, verification, and conversion across multiple funding sources so a customer can fund from anything they hold and the bank receives one asset.

→ Can customers fund in one asset and have the bank receive another? Yes. Any supported asset can be converted into the institution's preferred asset within the funding flow, so the bank can standardize on a stablecoin.

→ Is there an account funding API? Yes. Account funding is delivered as an account funding API and SDK, so a bank exposes one funding experience while the layer handles source connection, verification, and conversion.

→ What is funding source aggregation? Combining multiple funding sources within a customer's connected account — different tokens, or a linked cash balance — so a deposit can complete even when no single asset covers the full amount, which raises deposit success.

Related reading

- Verified Deposits: Wallet Ownership Verification for Banks

- Bank-to-Crypto Connectivity

- Digital Asset Infrastructure for Banks: The Operating Layer

- How SmartFunding Increases Crypto Deposit Success

- Mesh for Banking

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

%20(1).png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)