.svg)

.svg)

July 16, 2026

Verified Deposits: Confirm Wallet Ownership Before Funds Move

A bank can't accept what it can't attribute. When crypto arrives from an address no one can tie to a customer, it isn't really a deposit — it's exposure: unknown provenance, manual review, and the risk of freezing or unwinding funds after they land.

Verified deposits fix that at the source. Most crypto controls run after funds land — by the time a screen flags a problem, the exposure is already on the bank's books. Verified deposits move the check upstream: before any crypto moves, the customer proves they own the wallet or exchange account it's coming from — producing cryptographic proof of wallet ownership and an auditable trail — so every deposit enters the bank from a source it has verified, not one it has to investigate after the fact. Mesh provides the verification and the connectivity; the bank receives the assets, and Mesh is never in the flow of funds.

The result is the deposit experience clients already expect from traditional finance, without the compliance blind spot crypto usually brings.

Not legal or compliance advice. This page explains how the capability works and the regulatory context it maps to; validate against your own compliance and legal review.

Prove the customer owns the source — before funds move

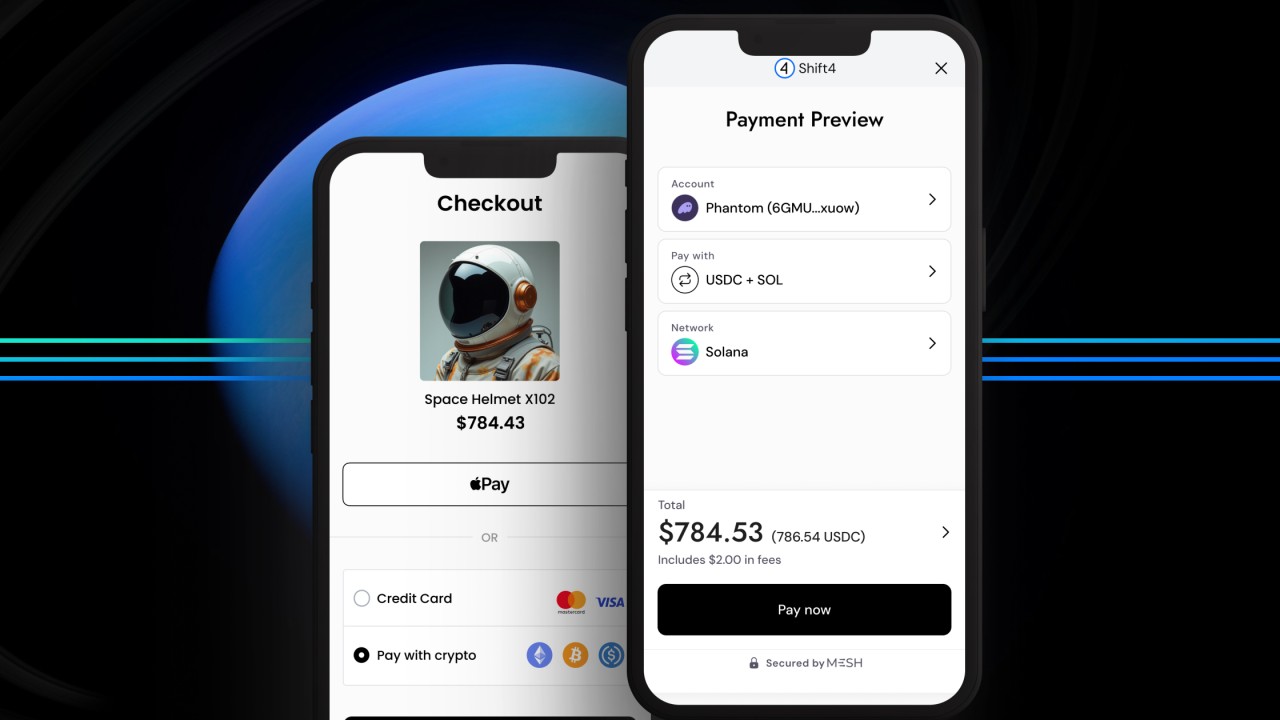

Every verified deposit answers one question before a single token moves: does this customer actually control the wallet or exchange account the funds are coming from? Mesh confirms it in seconds, then hands the bank a record it can keep.

For a self-custody wallet, the customer signs a one-time challenge message with their wallet — a method known as user attestation. It proves control without exposing a private key, moving funds, or paying gas, and returns wallet control verification the bank can audit: the address, the signed message, the signature hash, and a timestamp. For an exchange account, the customer authenticates the connection and the bank matches the account against the customer it already knows.

In a full deposit, that check is one of four stages Mesh runs inside the bank's own flow: counterparty authentication, wallet control verification, network and asset validation, and completion of the deposit in the bank's designated asset.

Every verification becomes compliance evidence

Wallet ownership verification isn't only about trust — it's about proof you can show a regulator. Each verified deposit produces an auditable link between a wallet and a client the bank has KYC'd — Mesh verifies the wallet; identity verification stays with the bank's own KYC process — which is exactly what transfer-compliance regimes are asking for. Under the EU's Transfer of Funds Regulation, institutions must assess whether a customer owns or controls a self-hosted wallet above €1,000 (see the EBA's Travel Rule Guidelines); both it and the US Bank Secrecy Act Travel Rule administered by FinCEN implement FATF's Recommendation 16. Verified deposits generate that evidence automatically, at the point of transfer — not after funds have already landed.

Cut the friction that loses deposits

The old way of accepting a crypto deposit leaks customers at every step: no more copying wallet addresses by hand, switching between external tools, or completing the multi-step verification the process historically required. Verified deposits keep the entire flow inside the bank's own experience — the customer picks a wallet, proves ownership, and funds in a few clicks. Fewer drop-offs means more secure crypto deposits actually completing, and more external crypto arriving as assets the bank holds.

You keep custody and control

Adopting verified deposits doesn't change how the bank holds assets. The institution stays in control of custody — holding assets itself or with its chosen custodian — while Mesh handles connectivity and verification and stays out of the flow of funds. Verification proves ownership; the deposit still lands with the bank, exactly as it would otherwise.

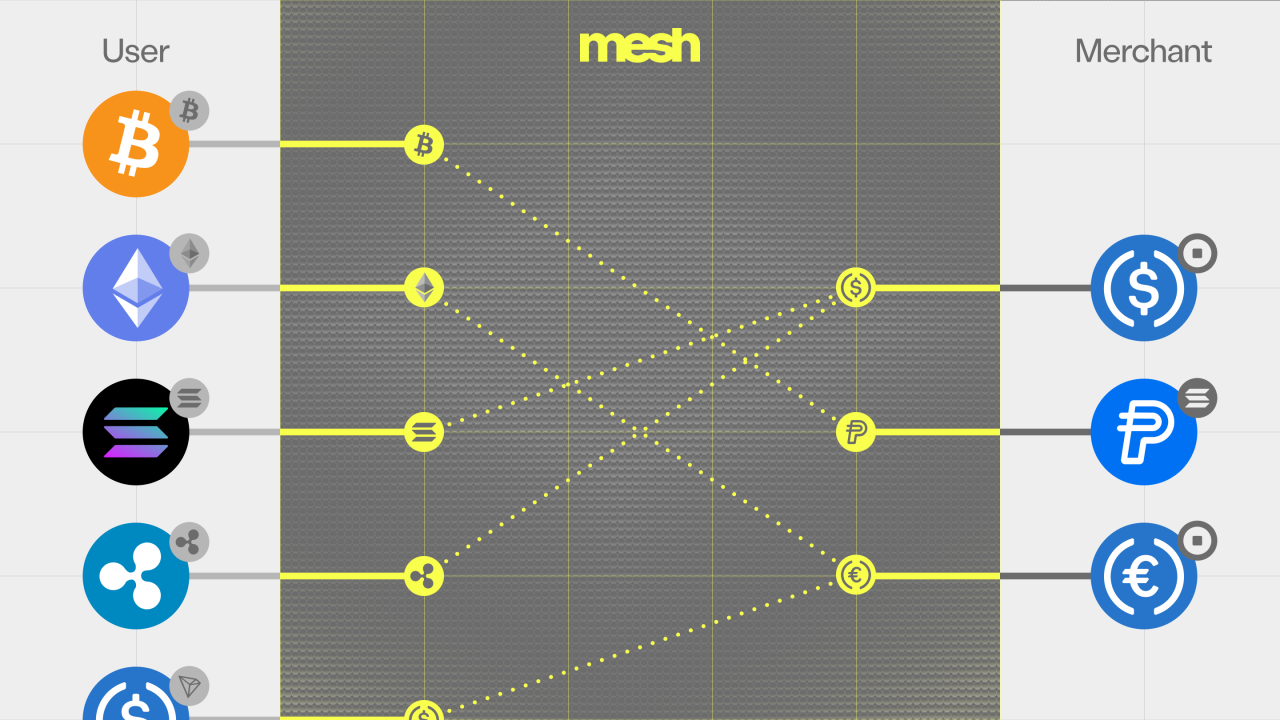

Built on Mesh's connectivity network

Verified deposits run across 300+ wallets and exchanges — the wallets (MetaMask, Phantom) and exchange accounts (Coinbase, Binance) customers already use — spanning 120+ tokens across 24 networks.

Proven with regulated institutions

AMINA Bank, the Swiss FINMA-regulated crypto bank, integrated Mesh for verified deposits — embedding them directly into its online banking platform so clients verify ownership and fund in one flow across hundreds of wallet providers.

Paxos, the regulated blockchain-infrastructure and tokenization platform, selected Mesh so the financial institutions it serves can offer verified ownership checks to their own customers before they deposit assets such as PYUSD and USDG, per its December 15, 2025 announcement. It's an example of how verified deposits can reach end users through a regulated infrastructure provider's institutional customer base.

Where verified deposits fit in your digital asset stack

Verified deposits are the compliance-critical first step — the same sequence AMINA has laid out publicly, starting here and extending to withdrawals and payouts. They sit on Mesh's bank-to-crypto connectivity and feed account funding, powered by SmartFunding. For the full picture, see digital asset infrastructure for banks.

Frequently asked questions

→ What are verified deposits? Crypto deposits a bank accepts only after wallet ownership verification (also called wallet control verification) confirms the customer owns or controls the source wallet or exchange account — producing an auditable proof record before funds move.

→ What is wallet ownership verification? A way of proving a customer controls a wallet, usually by having them sign a challenge message with the wallet's private key (a technique called user attestation). It proves control without exposing the key, moving funds, or paying gas.

→ Is wallet ownership verification required by regulation? In several jurisdictions, confirming control of a self-hosted wallet is part of transfer-compliance obligations above set thresholds (for example, €1,000 under the EU's Transfer of Funds Regulation, per the EBA Travel Rule Guidelines). These implement FATF Recommendation 16, the Travel Rule; US institutions operate under the Bank Secrecy Act Travel Rule. Confirm your obligations with compliance/legal.

→ Is there a wallet verification API? Yes. Banks integrate wallet ownership verification into their own deposit flow — embedded in the app or as a hosted verification step — so customers prove ownership in context instead of being sent to an external tool.

→ Does the customer pay gas or move funds to get verified? No. User attestation is gasless and proves control without an on-chain transaction.

Related reading

- Bank-to-Crypto Connectivity: How Banks Connect Customers to Wallets and Exchanges

- Account Funding for Banks: How Customers Fund an Account with Crypto

- Digital Asset Infrastructure for Banks: The Operating Layer

- What Is User Attestation? Proving Wallet Ownership Without Moving Funds

- Mesh for Banking

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

%20(1).png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)