.svg)

.svg)

July 16, 2026

Bank-to-Crypto Connectivity: How Banks Connect Customers to Wallets and Exchanges

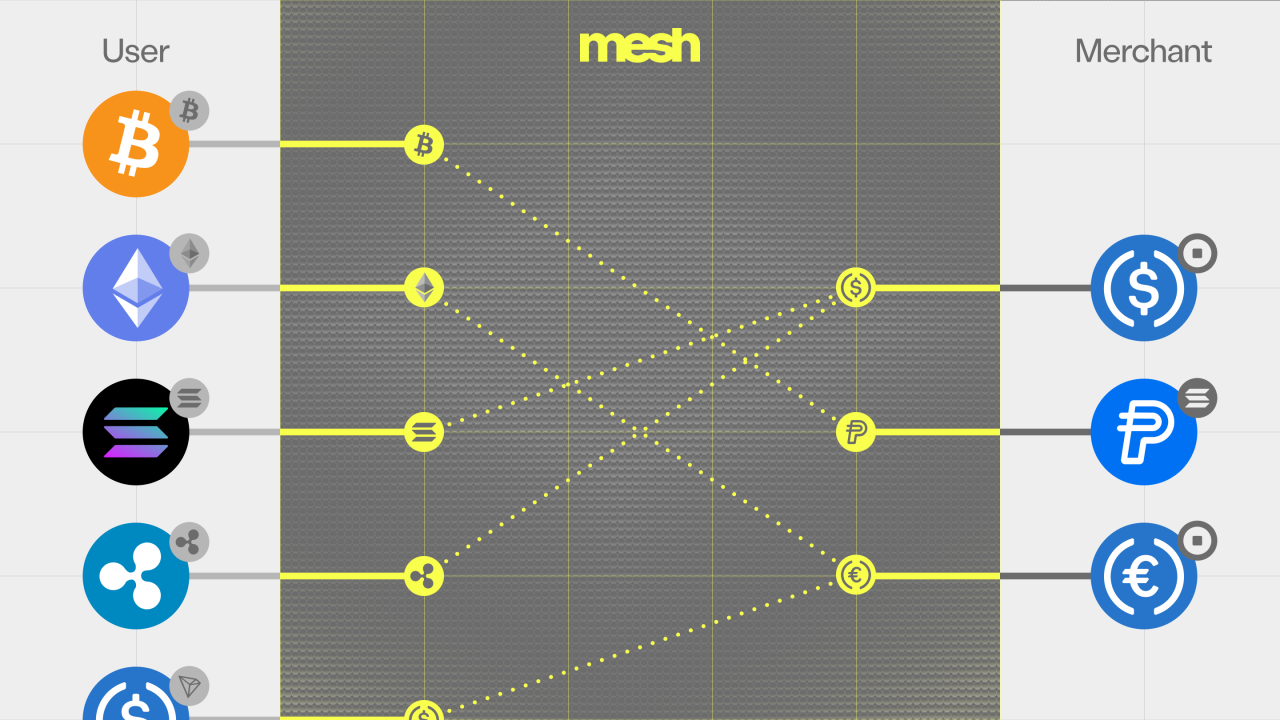

A bank doesn't need to become a crypto company to serve customers who already hold crypto — it needs a way to connect to where those assets live. Bank-to-crypto connectivity is a single integration that links a bank or neobank to the wallets and exchanges its customers already use — 300+ of them — so the institution can verify ownership, read balances and holdings, and let customers move assets in and out — all through one integration. Mesh provides this connectivity layer: one API in place of dozens of bespoke integrations, each maintained separately.

Banks often reach for a Plaid comparison — the layer that let fintechs connect to bank accounts through one integration. Connectivity plays that role for digital assets, but it's a floor, not a ceiling: the same layer also verifies ownership and orchestrates funding — things a data-connectivity tool doesn't.

Not legal or compliance advice. This article explains how the capability works. Requirements vary by jurisdiction and institution; validate against your own compliance and legal review.

What is bank-to-crypto connectivity?

Bank-to-crypto connectivity is infrastructure that connects a financial institution to its customers' external crypto accounts — self-custody wallets and exchange accounts — through one integration, so the institution can verify, read, and initiate movement of assets without building exchange or wallet infrastructure of its own. It is the plumbing beneath every customer-facing crypto feature a bank might launch: funding an account, verifying a deposit, showing a portfolio, or paying out. In short, it is how a bank can connect bank accounts to crypto — a capability also known as crypto account linking — through one interface instead of many.

The alternative is to build and maintain a separate integration to every wallet and exchange a customer might use — each with its own API, auth model, data format, and breaking changes. Connectivity infrastructure collapses that into a single interface with one integration to maintain.

What problem does connectivity solve for banks?

Customers already hold assets somewhere else, and banks have no standard way to reach them. A customer's crypto sits across Coinbase, Binance, MetaMask, Phantom, a hardware wallet like Ledger, or a dozen others. For a bank to let that customer fund an account, prove ownership, or view holdings, it has to speak to each of those platforms — a fragmented, high-maintenance engineering problem that most institutions cannot justify building in-house.

Connectivity solves three structural pains at once: coverage (reaching the long tail of wallets and exchanges without building each one), maintenance (one integration to keep current instead of dozens), and risk posture (reaching and verifying external accounts through one layer, without standing up new infrastructure to do it). The result is time-to-market measured in weeks rather than the quarters a from-scratch build would take.

How do banks connect to wallets and exchanges?

Connectivity spans two source types, because an exchange account and a self-custody wallet expose different things.

Exchange accounts. The customer authenticates a connection to their exchange account (for example, Coinbase or Binance). The connection itself verifies ownership — the institution confirms the account belongs to the customer it already knows — and enables reading balances and moving assets the customer approves.

Self-custody wallets. The customer connects MetaMask, Phantom, or another self-custody wallet. Ownership is verified with message signing — user attestation — a cryptographic proof that requires no fund movement and no gas.

In both cases, Mesh's role is connectivity and verification. When assets move, Mesh passes the customer's authenticated instruction to the platform that executes the transfer — funds move directly from source to destination, and Mesh is never in the flow of funds. It's the same model that underpins verified deposits: connect, verify, and enable movement.

What makes it different from building it in-house?

Coverage: one integration reaches 300+ wallets and exchanges, including the long tail a bank would never prioritize building itself. Every platform a bank can't reach is a customer funding somewhere else — coverage gaps are deposits left on the table. Maintenance transfer: keeping pace with each platform's API changes becomes the connectivity provider's job, not the bank's engineering backlog.

Which wallets, exchanges, and assets does it support?

Connectivity spans Mesh's network of 300+ wallets and exchanges — major exchange accounts (Coinbase, Binance, and others) and self-custody wallets (MetaMask, Phantom, and others) — across 120+ tokens and 24 networks.

Who is already using it?

AMINA Bank, the Swiss FINMA-regulated crypto bank, integrated Mesh for verified deposits — connecting its clients to hundreds of wallet providers directly inside its online banking platform, with ownership verified before deposits move.

Paxos, the regulated blockchain-infrastructure and tokenization platform, integrated Mesh so the institutions it serves can offer connectivity to external wallets and exchange accounts — with ownership verified before assets are deposited — to their own customers.

Where does connectivity fit in a bank's digital asset stack?

Connectivity is the foundation function of the operating layer described in digital asset infrastructure for banks. On top of it sit verified deposits (proving a customer controls a connected source before funds move) and account funding (aggregating and converting funds across sources). The engine that aggregates balances and converts assets behind the scenes is Mesh's funding engine, SmartFunding. For the full picture of how these layers assemble, see digital asset infrastructure for banks.

Frequently asked questions

→ What is bank-to-crypto connectivity? Infrastructure that connects a bank to its customers' external wallets and exchange accounts through one integration, so the bank can verify ownership, read balances, and enable asset movement, with Mesh itself never taking custody.

→ Can a bank connect to Coinbase, Binance, or MetaMask? Yes. Connectivity spans 300+ wallets and exchanges, including major exchange accounts and self-custody wallets. Available data and actions vary by platform, region, and account tier.

→ How is ownership verified? For self-custody wallets, via message signing (user attestation) — a cryptographic proof that requires no fund movement or gas. For exchange accounts, via an authenticated connection and data matching.

→ How long does it take to launch? One integration replaces dozens, so time-to-market is typically weeks rather than the quarters a from-scratch build would require.

Related reading

- Verified Deposits: Wallet Ownership Verification for Banks

- Account Funding for Banks

- Digital Asset Infrastructure for Banks: The Operating Layer

- What Is User Attestation? Proving Wallet Ownership Without Moving Funds

- How SmartFunding Orchestrates Any-to-Any Funding

- Mesh for Banking

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

%20(1).png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)