.svg)

.svg)

.png)

July 16, 2026

How AMINA Bank and Mesh Bring Verified Digital Asset Deposits to Regulated Banking

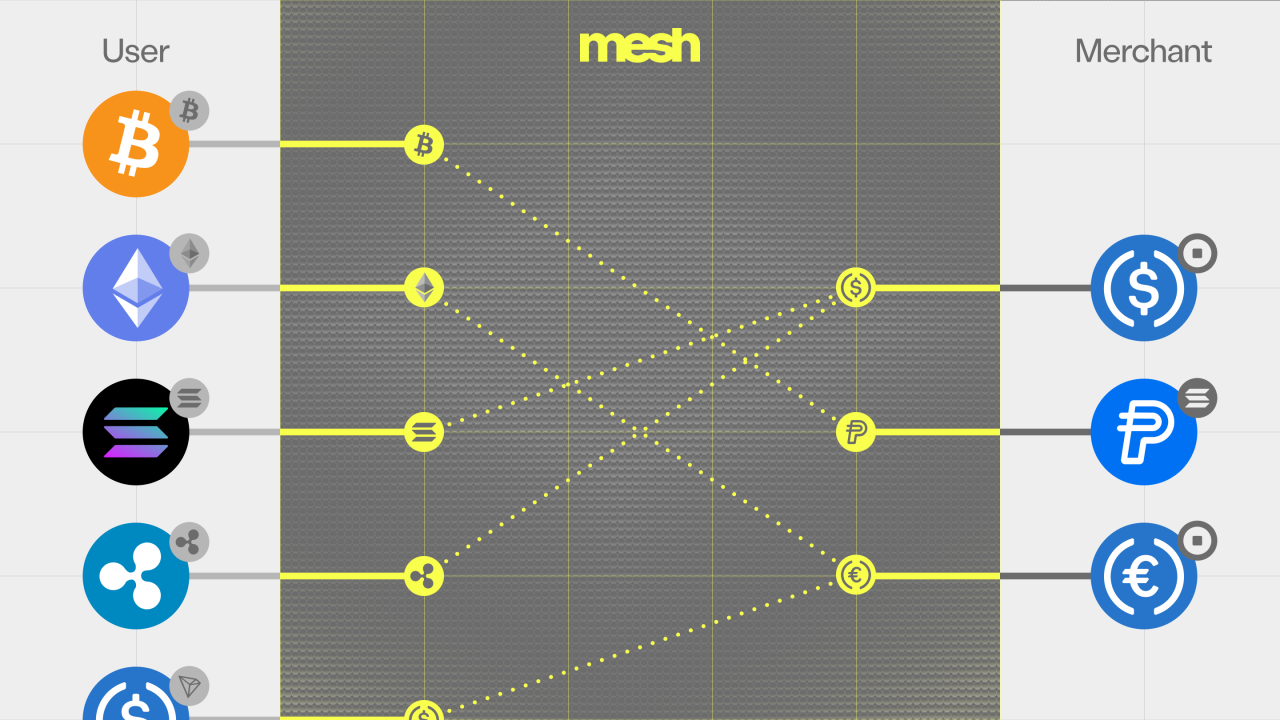

AMINA Bank AG — a Swiss Financial Market Supervisory Authority (FINMA)-regulated crypto bank headquartered in Zug — is the first regulated bank to integrate Mesh. The integration embeds Mesh's verified deposit technology directly into AMINA's online banking platform, so clients can verify wallet ownership and deposit stablecoins and digital assets in a single, streamlined flow across more than 300 wallet providers (per the joint announcement, July 2026).

What is the AMINA Bank–Mesh partnership?

The AMINA Bank–Mesh partnership makes AMINA the first FINMA-regulated bank to integrate Mesh, the crypto payments network, embedding wallet ownership verification and digital asset deposits directly into the bank's online banking platform (per the joint announcement, July 2026). AMINA, founded in Zug in 2018 and licensed by FINMA as a Swiss bank and securities dealer in 2019, operates at the intersection of traditional banking and digital assets, serving professional investors, corporations, and financial institutions from regulated hubs in Switzerland, Abu Dhabi (ADGM), and Hong Kong (SFC) (per AMINA's corporate material. Mesh provides the verification and connectivity layer; AMINA receives and custodies the deposited assets within its Swiss regulated banking environment.

What does the integration let AMINA clients do?

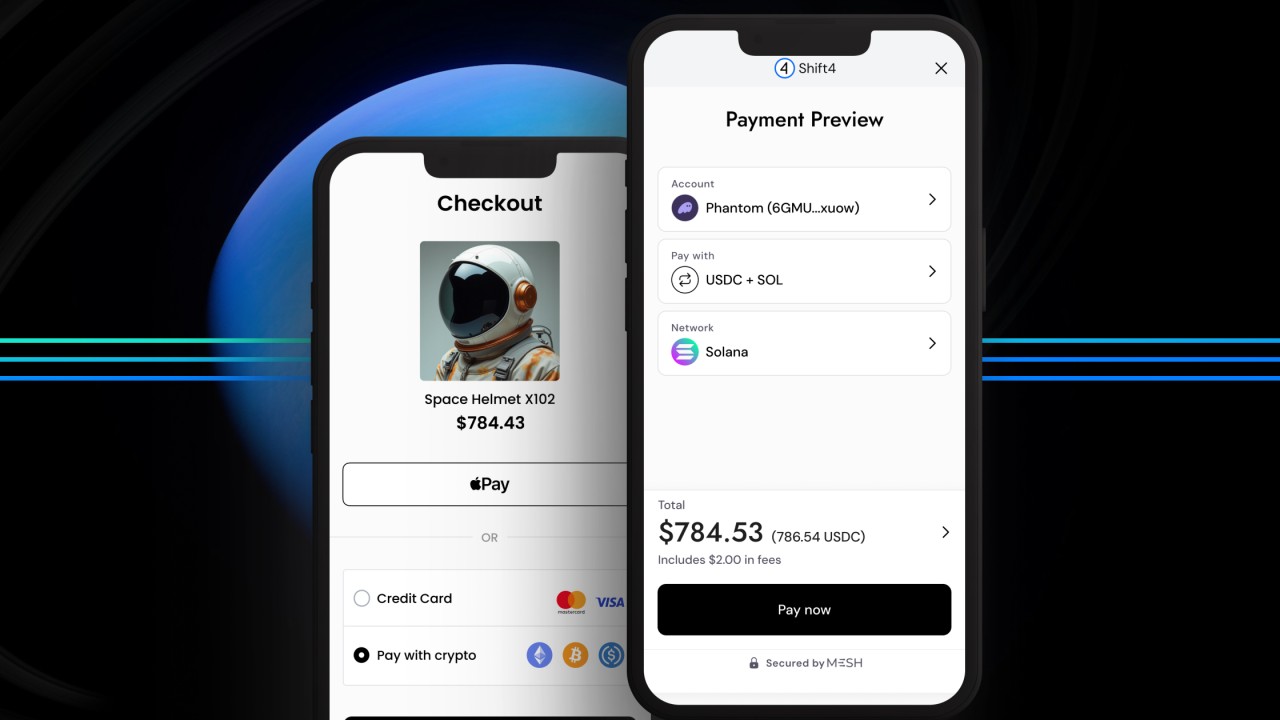

AMINA clients can deposit stablecoins and digital assets into their bank account from their existing wallets and exchange accounts — selecting their wallet provider, verifying ownership, and depositing within AMINA's platform in a few clicks (per Myles Harrison, Chief Product Officer at AMINA, in the announcement). There is no more copying wallet addresses by hand, switching between external tools, or completing the multi-step verification the process historically required.

Before this integration, depositing into a bank required clients to complete wallet-signing on external platforms and verify addresses through multi-step manual processes (per Harrison's statement). The integration brings the digital asset deposit experience in line with the standards clients expect in traditional finance — inside the bank's own interface, under the bank's own compliance framework.

How does Mesh power AMINA's verified deposits?

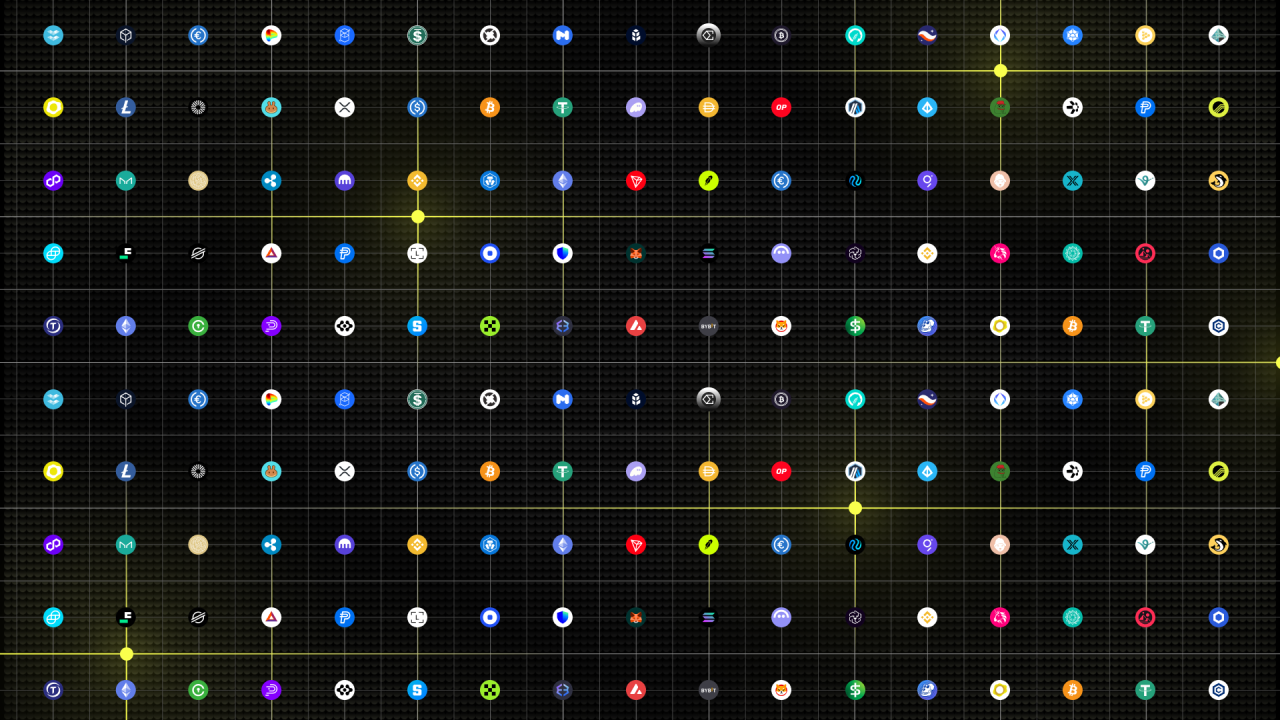

The flow combines two Mesh capabilities in one session. Mesh's wallet ownership verification solution cryptographically confirms that the client controls the external wallet — the client connects the wallet and signs an ownership message — before any funds reach the bank. Mesh's deposit connectivity then links the client's verified wallet or exchange account to their AMINA account, across a network of more than 300 wallets and exchanges.

The architecture reflects how Mesh works with every regulated institution: Mesh is an orchestration and instruction layer. It passes the client's authenticated instructions and ownership proof to the bank and is never in the flow of funds — verification and connectivity only. AMINA receives and custodies deposited assets, applying its own compliance and on-chain screening infrastructure natively within its regulated environment.

Why does this matter for regulated banking?

Demand for regulated digital asset infrastructure has outrun supply. According to Bessemer Venture Partners, real-world stablecoin payments doubled in 2025 to $400 billion even as broader crypto markets declined, with 60% of that volume driven by B2B flows — corporate treasury, cross-border settlement, and payment service providers clearing transactions for their clients (as cited in the joint announcement). The demand is there, but the regulated banking infrastructure to support it has not kept pace. AMINA's integration of Mesh closes that gap, connecting clients directly to their existing wallets and exchange accounts within a Swiss regulated banking environment.

"As the first FINMA-regulated bank to integrate Mesh, AMINA is proving how digital assets can move through regulated finance — verification and compliance handled natively," said Bam Azizi, Co-Founder and CEO of Mesh, in the announcement. "We're proud to provide the connectivity that makes it possible."

The partnership also matters beyond AMINA's own client base. Through AMINA's B2B2C platform, financial institutions can access Mesh's connectivity through AMINA's regulated banking framework, with compliance and on-chain screening infrastructures already in place (per Dr. Sebastian Preil, Global Head of B2B2C and Managing Director at AMINA, in the announcement). For any regulated institution entering crypto, that answers a practical challenge Preil names directly: how to verify a client's on-chain footprint alongside their traditional financial profile.

Which assets and platforms does it support?

The integration connects AMINA clients to their wallets and exchange accounts across more than 300 providers in Mesh's network. AMINA's platform supports stablecoins and digital assets including USDC, USDT, and other major assets.

What's next for the partnership?

The integration will soon be available for AMINA clients, with additional capabilities expected later in 2026. AMINA has stated that verified deposits are the first step, with intent to extend Mesh's connectivity to withdrawals and payouts in the future, as it builds the infrastructure through which stablecoins and digital assets could move at scale (per Harrison's statement).

Partnership history

AMINA Bank and Mesh announced the integration in July 2026 via a joint release (Businesswire). AMINA received its Swiss banking and securities dealer licence from FINMA in 2019 (founded as SEBA Bank in 2018, rebranded AMINA in late 2023) and holds regulatory permissions in Abu Dhabi (ADGM/FSRA, 2022) and Hong Kong (SFC, 2023), per AMINA's corporate material

Frequently asked questions

→ What is the AMINA Bank–Mesh integration? AMINA Bank, a FINMA-regulated Swiss crypto bank, is the first regulated bank to integrate Mesh. The integration embeds Mesh's verified deposit technology into AMINA's online banking platform, letting clients verify wallet ownership and deposit stablecoins and digital assets in one streamlined flow across 300+ wallet providers.

→ Does Mesh custody the deposited assets? No. Mesh provides verification and connectivity only and is never in the flow of funds. AMINA receives and custodies deposited assets within its Swiss regulated banking environment.

→ How is wallet ownership verified? Through Mesh's verification solution, the client connects their wallet and signs an ownership message, cryptographically proving control of the address before funds reach the bank — all within AMINA's platform.

→ Which platforms can AMINA clients deposit from? Clients can connect wallets and exchange accounts across Mesh's network of more than 300 providers, subject to AMINA's approved platform list.

→ Can other financial institutions use this? Through AMINA's B2B2C platform, financial institutions can access Mesh's connectivity through AMINA's regulated banking framework, per AMINA's announcement. Institutions can also work with Mesh directly.

Related reading

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

%20(1).png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)